How stocks correlation, Grayscale, Russia, stablecoins, rate hikes and more are impacting the bitcoin price today.

Listen To This Episode:

AppleSpotifyGoogleLibsynOvercast

In this episode of Bitcoin Magazine‘s “Fed Watch: podcast, CK and I continued our monthly series with Dylan LeClair, author of the Deep Dive report. We had the opportunity to go over the metrics in the bitcoin market that he is watching and is an expert in. They have a free version of the report that comes out daily, and an exclusive paid version monthly and yearly. Follow along with his slide deck here.

“Fed Watch” is a podcast for people interested in central bank current events. Bitcoin will consume central banks one day, understanding and documenting how that is happening is what we are about here at “Fed Watch.”

The first topic we covered in this episode and the first topic from the January issue of the Deep Dive is bitcoin’s correlation to stocks and the volatility measure, the VIX. LeClair described why this correlation has appeared over the last year and what it can tell us about the health of the bitcoin market.

Source: January 2022 Deep Dive

Source: January 2022 Deep Dive

One of the bigger topics we talked about with LeClair was Grayscale and the effect this market behemoth has on the bitcoin price.

Source: January 2022 Deep Dive

As you can see in the chart above, GBTC inflows abruptly stopped in January 2021, one year before this report, and interestingly, very near the price of bitcoin at the time of this writing of $42,000.

LeClair walked us through this product and its effect on the market. We talked about major institutions, aka market makers, that could have been caught on the wrong side of this trade, as the large price premium that was facilitating “risk free” arbitrage suddenly changed to a discount.

Source: Slide deck of February 2022 Deep Dive

As the name suggests, the Deep Dive is an in-depth report that goes into very specific metrics about the Bitcoin network. One of those is what I interpret as the liquidity of circulating supply and its correlation to price. As you can see in the chart above, the shaped areas represent coins that have moved within a three-month period. It is related to velocity, but where velocity is concerned with the number of transactions, liquidity of circulating supply is a percent of the total supply that has moved at least once.

The percentage of supply that becomes liquid begins to ramp up as the price approaches peaks, and resets lower as price consolidates. The pattern is emerging of lower top-level circulating supply and lower lows. That makes sense if we think in terms of purchasing power at the tops and bottoms. In other words, each peak is a lower number of satoshis but a higher level of purchasing power, since the price is significantly higher. And vice versa, the lows are a lower number of satoshis but a higher level of purchasing power.

If bitcoin is going to continue appreciating in value, we would expect that exact pattern to continue. As new entrants come into the market they will find fewer satoshis to buy, even in times of FOMO.

The next part of our discussion blew me away. LeClair discussed the rise of stablecoins like Tether that are growing in use as collateral for leveraged trades in bitcoin. In the past, people tended to use their bitcoin as collateral, which acted to accentuate price moves. With stablecoins taking more of that role, it should lead to much less volatility in the bitcoin price.

LeClair also mentioned the fact that Tether and other stablecoins provide small, much noticeable buy pressure for U.S. government securities. They have these very large reserves of dollars that they need to put into safe assets. What’s better for this than U.S. treasuries?

I make a connection that the typical list of foreign holders of U.S. government debt should be expanded to include, not just foreign central banks, but perhaps in the future, companies like Tether. How crazy would it be to see Tether with just as many U.S. treasuries as countries like Germany, China or Japan? This would instantly make Tether and other stablecoins massive geopolitical players.

On the day of recording this live stream, March 1, 2022, bond markets were swinging wildly. So, we examined just what was happening and gave our listeners some expectations for the rest of the year.

The chart below shows the odds of a 50 basis point (bps) hike this month are now zero, and the odds of any hike continue to drop. The number of implied rate hikes by the end of the year has fallen from nearly seven to now less than five. I suspect that it will continue to fall over the next few months to at most three rate hikes in 2022.

Source: Zerohedge

We ended the episode with some talk about the situation in Russia and Ukraine, as regards to the sanctions of the SWIFT network. The only viable alternative on the horizon is Bitcoin. The much discussed Russia/China alternative is in its infancy and still uses banks as nodes which are vulnerable to sanctions. Gold is not an option for quick international settlement, and will likely suffer price declines in this situation because Russia needs to access dollars, and can sell gold to do that.

The Russia/China interbank alternative is not an alternative banking or financial system, it is just a messaging protocol. It is in the same boat as a central bank digital currency (CBDC), it’s new but not revolutionary. It still has all the points of failure like corrupt institutions and rails of the past. Bitcoin, on the other hand, is fundamentally a new system, with a new monetary unit. It is the only thing at this time that fits the bill as an alternative to SWIFT and the decrepit fiat system.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Listen To This Episode:

AppleSpotifyGoogleLibsynOvercast

In this episode of Bitcoin Magazine‘s “Fed Watch: podcast, CK and I continued our monthly series with Dylan LeClair, author of the Deep Dive report. We had the opportunity to go over the metrics in the bitcoin market that he is watching and is an expert in. They have a free version of the report that comes out daily, and an exclusive paid version monthly and yearly. Follow along with his slide deck here.

“Fed Watch” is a podcast for people interested in central bank current events. Bitcoin will consume central banks one day, understanding and documenting how that is happening is what we are about here at “Fed Watch.”

The first topic we covered in this episode and the first topic from the January issue of the Deep Dive is bitcoin’s correlation to stocks and the volatility measure, the VIX. LeClair described why this correlation has appeared over the last year and what it can tell us about the health of the bitcoin market.

One of the bigger topics we talked about with LeClair was Grayscale and the effect this market behemoth has on the bitcoin price.

As you can see in the chart above, GBTC inflows abruptly stopped in January 2021, one year before this report, and interestingly, very near the price of bitcoin at the time of this writing of $42,000.

LeClair walked us through this product and its effect on the market. We talked about major institutions, aka market makers, that could have been caught on the wrong side of this trade, as the large price premium that was facilitating “risk free” arbitrage suddenly changed to a discount.

As the name suggests, the Deep Dive is an in-depth report that goes into very specific metrics about the Bitcoin network. One of those is what I interpret as the liquidity of circulating supply and its correlation to price. As you can see in the chart above, the shaped areas represent coins that have moved within a three-month period. It is related to velocity, but where velocity is concerned with the number of transactions, liquidity of circulating supply is a percent of the total supply that has moved at least once.

The percentage of supply that becomes liquid begins to ramp up as the price approaches peaks, and resets lower as price consolidates. The pattern is emerging of lower top-level circulating supply and lower lows. That makes sense if we think in terms of purchasing power at the tops and bottoms. In other words, each peak is a lower number of satoshis but a higher level of purchasing power, since the price is significantly higher. And vice versa, the lows are a lower number of satoshis but a higher level of purchasing power.

If bitcoin is going to continue appreciating in value, we would expect that exact pattern to continue. As new entrants come into the market they will find fewer satoshis to buy, even in times of FOMO.

The next part of our discussion blew me away. LeClair discussed the rise of stablecoins like Tether that are growing in use as collateral for leveraged trades in bitcoin. In the past, people tended to use their bitcoin as collateral, which acted to accentuate price moves. With stablecoins taking more of that role, it should lead to much less volatility in the bitcoin price.

LeClair also mentioned the fact that Tether and other stablecoins provide small, much noticeable buy pressure for U.S. government securities. They have these very large reserves of dollars that they need to put into safe assets. What’s better for this than U.S. treasuries?

I make a connection that the typical list of foreign holders of U.S. government debt should be expanded to include, not just foreign central banks, but perhaps in the future, companies like Tether. How crazy would it be to see Tether with just as many U.S. treasuries as countries like Germany, China or Japan? This would instantly make Tether and other stablecoins massive geopolitical players.

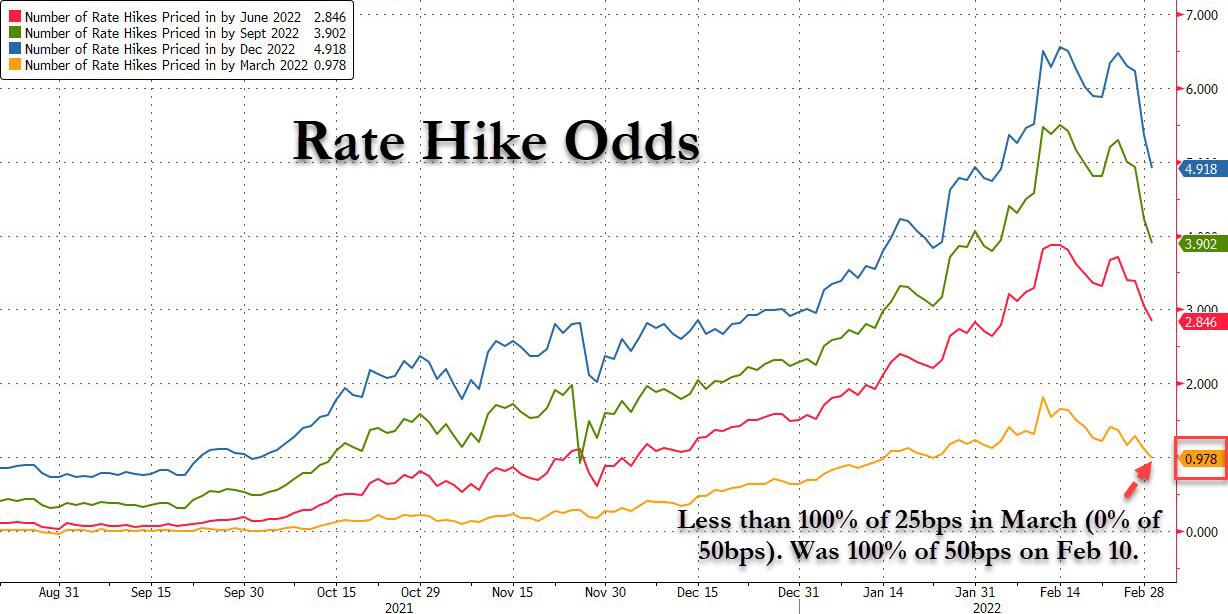

On the day of recording this live stream, March 1, 2022, bond markets were swinging wildly. So, we examined just what was happening and gave our listeners some expectations for the rest of the year.

The chart below shows the odds of a 50 basis point (bps) hike this month are now zero, and the odds of any hike continue to drop. The number of implied rate hikes by the end of the year has fallen from nearly seven to now less than five. I suspect that it will continue to fall over the next few months to at most three rate hikes in 2022.

We ended the episode with some talk about the situation in Russia and Ukraine, as regards to the sanctions of the SWIFT network. The only viable alternative on the horizon is Bitcoin. The much discussed Russia/China alternative is in its infancy and still uses banks as nodes which are vulnerable to sanctions. Gold is not an option for quick international settlement, and will likely suffer price declines in this situation because Russia needs to access dollars, and can sell gold to do that.

The Russia/China interbank alternative is not an alternative banking or financial system, it is just a messaging protocol. It is in the same boat as a central bank digital currency (CBDC), it’s new but not revolutionary. It still has all the points of failure like corrupt institutions and rails of the past. Bitcoin, on the other hand, is fundamentally a new system, with a new monetary unit. It is the only thing at this time that fits the bill as an alternative to SWIFT and the decrepit fiat system.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Feedzy

In El Salvador, about two hours away from the capital, up in the mountains, lies…

Bitcoin has experienced a challenging period recently, with its price consistently declining over the past…

U.S. inflation unexpectedly marched higher in January, sending crypto and traditional markets sharply lower. The…

World Liberty Financial (WLFI), a crypto project Trump has financial interests in, has launched a…

By Francisco Rodrigues (All times ET unless indicated otherwise) The U.S. inflation report due later…

Crypto markets slid 3% in the past 24 hours as traders await U.S. consumer price…

{kind=link}